Introduction: The Bellwether Status of Cisco in an AI-Driven Market

For years, investors treated cisco stock as a steady but boring networking play. That view has flipped in 2026. Cisco has become one of the most exciting names in the AI infrastructure race, and its stock moves now tell us a lot about where the entire tech sector is heading.

Here’s the thing. In fiscal Q2 2026, Cisco reported revenue of $15.3 billion, a 10% jump from the prior year, driven by strong demand for AI networking gear. But the headline number that really caught everyone’s attention came a few months earlier: AI orders surged past $1.3 billion in a single quarter. This isn’t just about selling more routers and switches. Cisco is now a key piece of the AI backbone, providing the networking equipment that makes massive data centers actually work.

When a company like Cisco posts strong earnings and raises its full-year guidance, it signals something bigger. Enterprise spending is healthy. AI monetization is real, not just hype. That’s why Cisco is considered a bellwether for the broader tech market. If you track cisco stock, you get a useful read on trends that also affect other major names, from alphabet stock to jnj stock and even speculative stories like gamestop stock.

In fact, Cisco has been one of the biggest movers in big tech stocks today.

But keeping up with all these moving pieces is tough. You need clear, daily insights to separate the real signal from the noise. That’s exactly why The Deep View Newsletter exists. It delivers straightforward AI and tech updates straight to your inbox, no hype attached.

Cisco’s AI Infrastructure Pivot and Its Revenue Impact

Cisco did not stumble into the AI boom by accident. The company spent years building custom chips called Silicon One and a platform called Nexus Hyperfabric. These products are not your standard networking gear. They are built for the fast, heavy data loads that AI models need to run.

That shift is now showing up in the numbers. In fiscal Q2 2026, Cisco reported revenue of $15.3 billion, a 10% jump from the prior year. The main driver? Demand for AI-ready networking equipment. Companies building giant AI clusters need Cisco’s gear to make everything talk to each other.

But the real eye-opener came earlier in the year. In fiscal Q1 2026, AI-related product orders surged past $1.3 billion in a single quarter. That was a huge leap. Investors who track cisco stock saw that number and realized Cisco was not just a boring networking company anymore. It was becoming a core part of the AI infrastructure story.

Cisco’s own guidance backs this up. The company now expects full-year fiscal 2026 revenue to land between $62.8 billion and $63.0 billion. That is a strong outlook, and it tells you that enterprise AI spending is real and growing.

How does Cisco compare to other AI hardware players like Nvidia? Nvidia sells the brains of the AI operation, the GPUs. Cisco sells the nervous system, the networking that connects everything. You cannot have one without the other. That is what makes Cisco a unique and powerful bet in the AI space right now.

For investors watching the biggest movers today in big tech stocks, Cisco’s pivot is a signal you cannot ignore. It shows that legacy companies with deep enterprise relationships can reinvent themselves.

If you are building a portfolio around AI, Cisco deserves a close look alongside more obvious picks. In fact, tracking how Cisco performs alongside other enterprise tech giants gives you a much clearer picture of where the sector is headed.

Keeping up with all of these moving parts takes time. You need a source that cuts through the hype and tells you what actually matters. That is exactly why The Deep View Newsletter exists. It delivers clear, daily AI and tech updates straight to your inbox. No fluff, just insights you can use.

Earnings Report Analysis: Key Metrics and Guidance Driving the Stock

Let’s walk through the actual numbers that moved cisco stock in 2026. This is where the story gets really interesting for anyone tracking big tech stocks.

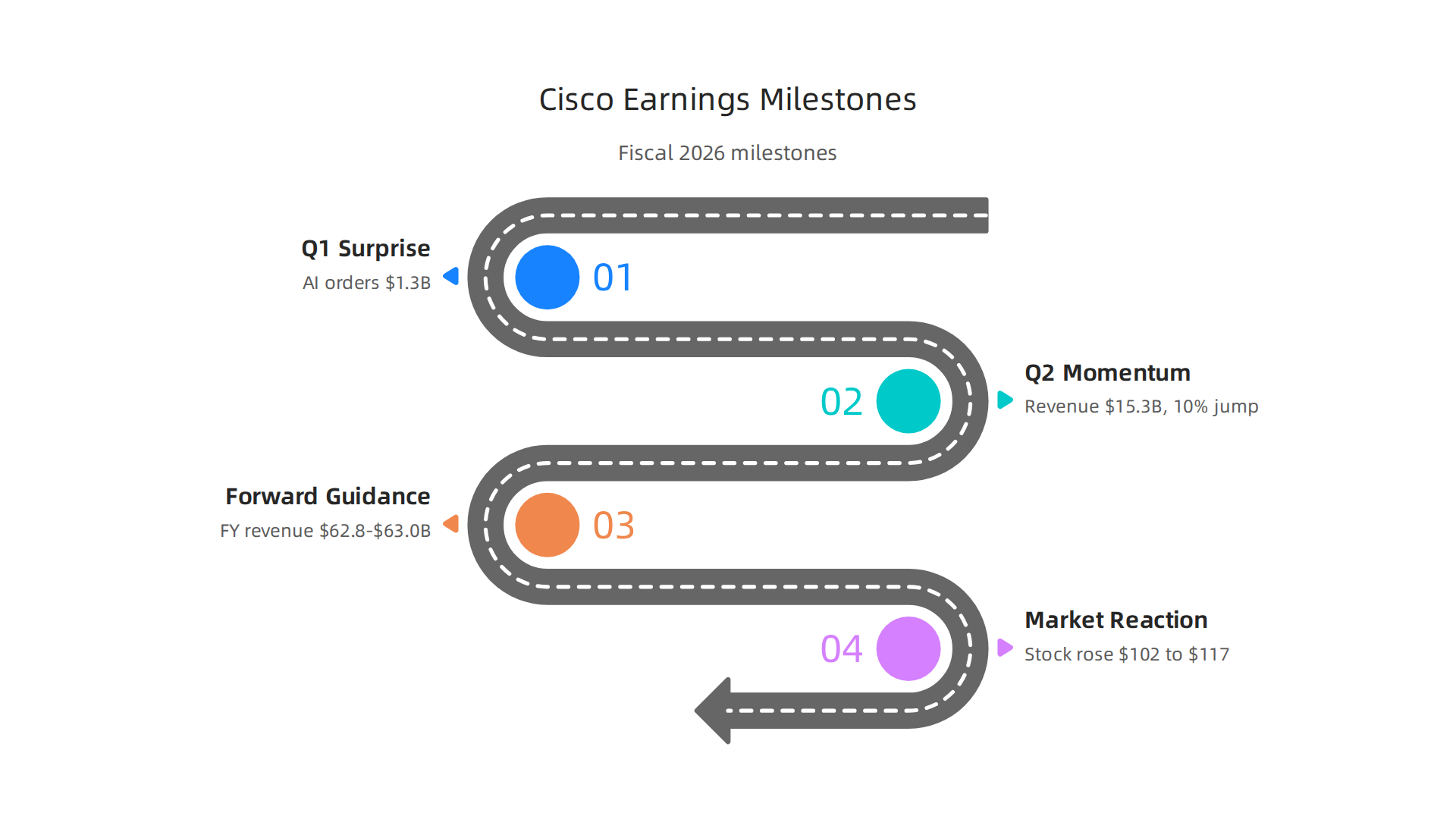

The Q1 surprise. In November 2025, Cisco kicked off fiscal 2026 with a bang. The company delivered better-than-expected profit and revenue in the first quarter, and the headline number that grabbed everyone’s attention was $1.3 billion in AI-related orders. That single data point told investors that the AI pivot was not just talk. It was real revenue.

Q2 kept the momentum going. By February 2026, Cisco reported second quarter revenue of $15.3 billion, a 10% jump from the prior year. The company’s own guidance had called for $15 billion to $15.2 billion, so they beat their own forecast. That is the kind of consistency that builds confidence in a stock.

Forward guidance sealed the deal. In May 2026, Cisco reported third quarter earnings and raised its full-year outlook. The company now expects fiscal 2026 revenue to land between $62.8 billion and $63.0 billion. For context, HSBC nearly doubled its price target for cisco stock, moving from $77 to $137 in a single note. That kind of analyst upgrade does not happen often.

The market reacted fast. After the Q1 report, cisco stock started climbing. By May 2026, the stock jumped from around $102 to above $117 in pre-market trading after the Q3 earnings release. It then settled into a tight range between $114 and $117. The options market also saw big implied moves, signaling that traders expected volatility.

To put this in perspective, comparing Cisco’s trajectory to other enterprise tech plays like alphabet stock or jnj stock shows a similar pattern of steady growth fueled by structural demand. Even high-volatility names like gamestop stock can teach us something about market sentiment, but Cisco’s story is about real fundamentals.

Here is the bottom line. Cisco is beating expectations, raising guidance, and seeing its stock re-rated by analysts. If you are trying to track cisco stock alongside other big tech movers, you need a clear view of all the earnings data.

Keeping up with earnings reports across multiple companies takes serious effort. That is why The Deep View Newsletter delivers clear daily AI and tech updates straight to your inbox. No fluff, just the insights you need to make informed decisions.

Competitive Landscape: Cisco vs. Arista vs. Juniper

The earnings story matters, but here is the real question for anyone tracking cisco stock: Can Cisco hold its ground as rivals eat into its core networking business?

The answer is a mix of strength and threat.

Market share shifts are real. Cisco still leads the overall Ethernet switch market with roughly 29.8% share, but it is losing ground, according to a recent report from SDxCentral.

Meanwhile, Arista has captured 12.6% of the total market and a more impressive 19% share in the datacenter segment, as noted by IDC. And Juniper, now part of HPE, adds another aggressive contender. The global Ethernet switch market is projected to grow from $46.22 billion in 2026 to $76.4 billion by 2034, so there is plenty of room for multiple winners.

Revenue growth and margins tell a two-sided story. Cisco benefits from its enormous installed base and diversified revenue streams, but its networking segment faces margin pressure from cheaper white box switches. Arista runs with industry-leading gross margins around 60% thanks to its software-driven approach. Juniper/HPE focuses on high-performance routing for service providers. This competitive pressure is a key reason why analysts factor in both the AI tailwind and market share erosion when valuing cisco stock.

The product innovation race is heating up. Cisco pushes its custom Silicon One chips to power AI data centers, while Arista counters with its 7130 series built for low latency. Juniper’s PTX series targets massive core routing. The battle is not just about speed; it is about which architecture scales best for AI workloads.

For investors comparing tech ecosystems, understanding these dynamics is as critical as studying the earnings of alphabet stock or the defensive positioning of jnj stock. The networking wars will directly shape cisco stock performance in the next few years.

Want to stay ahead of these shifts? The Deep View Newsletter delivers clear daily updates on the companies that power the internet, minus the noise.

Enterprise Networking Spending Trends in 2026

Here is a question worth asking if you track cisco stock: Where are enterprise IT budgets actually going in 2026?

The answer is clearer than ever. Companies are shifting big portions of their networking spend toward AI-enabled infrastructure and tighter security. The global Ethernet switch market is projected to grow from $46.22 billion in 2026 to $76.4 billion by 2034, according to Fortune Business Insights. That growth is not just about adding more ports. It is about buying smarter, AI-ready hardware.

Cisco still leads the Ethernet switch market with roughly 29.8% share, per a recent report from SDxCentral. But the bigger story is how Cisco’s end-to-end portfolio gives it an edge that pure-play rivals cannot match. When a company needs routing, switching, security, and observability from one vendor, Cisco delivers a complete stack. That bundling advantage matters more as IT teams work to simplify their supply chains.

Adoption patterns differ by company size. Large enterprises are leading the charge on Cisco’s AI-powered Catalyst and Meraki platforms. These buyers have the budgets and the IT teams to run complex AI workloads. Small and midsize businesses move slower. They tend to stick with older hardware or choose simpler cloud-managed options from Meraki.

This shift in enterprise spending directly affects cisco stock performance. More budget allocated to AI networking means more revenue per customer. And as companies like Alphabet and Johnson & Johnson push deeper into AI infrastructure, their networking needs grow too. Meanwhile, gamestop stock moves on retail sentiment, but cisco stock depends on real enterprise demand.

For investors who want to track these budget shifts clearly, learning how to filter Yahoo Finance news for big tech market insights can help cut through the noise.

Want to stay current on these spending trends? The Deep View Newsletter delivers clear daily updates on the companies powering the internet, minus the hype.

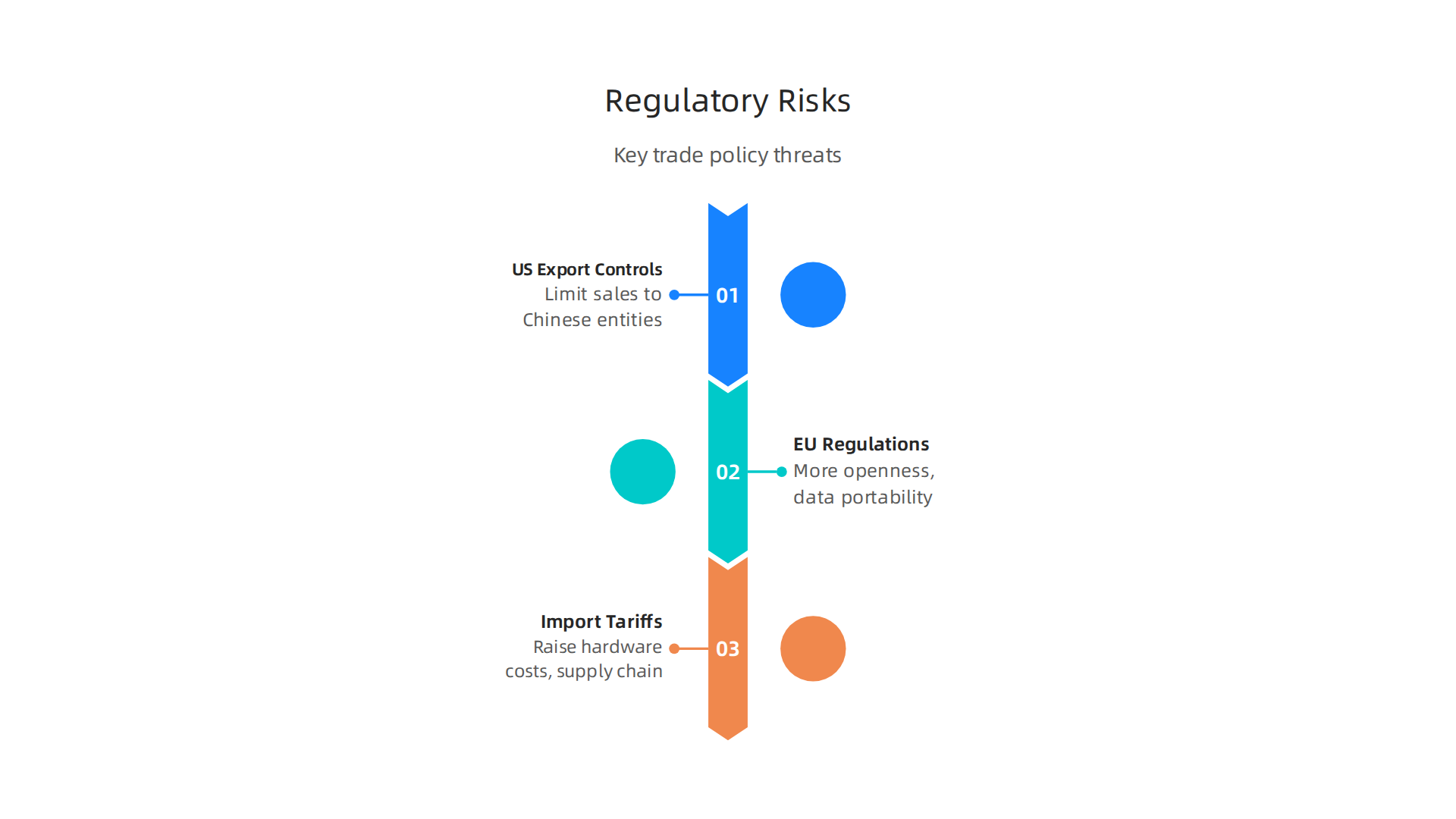

Regulatory and Trade Policy Risks

Trade policies and regulations may not grab headlines like a new product launch. But for Cisco investors, these rules matter a lot.

They can cut into revenue, raise costs, and slow down growth.

Here are the three biggest policy risks to watch in 2026.

First, US export controls on semiconductor equipment create real exposure for Cisco. The company still generates meaningful revenue from China. New rules that limit the sale of advanced computing and semiconductor gear to Chinese entities directly affect Cisco’s ability to sell networking hardware there. A 2022 regulation expanded controls on high-performance chips and supercomputer tech, according to K&L Gates. While 2026 has seen a cooling in new export rules amid ongoing US-China trade talks, as East Asia Forum reports, the risk has not gone away. Any escalation could hurt Cisco’s China business fast.

Second, the EU’s Digital Markets Act and Data Act put pressure on Cisco’s cloud networking business. These rules require more openness and data portability. They could force Cisco to change how it bundles products in Europe. That means higher compliance costs and possible limits on how the company sells its integrated stack. For a company that wins by selling full solutions, this is a real headwind.

Third, tariffs on imported components threaten Cisco’s supply chain. The company sources parts from many countries. New tariffs on semiconductors, metals, or finished electronics would raise hardware costs. Cisco has been diversifying its supply chain for years, but no company is immune to broad tariff increases.

For investors looking to track how these regulatory shifts affect cisco stock over time, learning to stop chasing noise and monitor stock moves with a repeatable framework can make a real difference.

Want to stay ahead of regulatory risks without the noise? The Deep View Newsletter sends clear daily updates on the policies shaping big tech.

Technical Analysis: Cisco Stock Chart Patterns and Key Levels

Looking at the price chart of cisco stock (CSCO) in 2026 tells a clear story of momentum. But the numbers also show some risks for short-term traders.

First, the big picture. Cisco has been on a strong run. The stock surged nearly 99% since 2024, according to TheStreet. That performance beats the overall market. But when a stock moves that fast, you need to watch the technical signals.

The 50-day simple moving average (SMA) is the short-term trend line. The 200-day SMA shows the long-term trend. Cisco stock has stayed well above both for months. That is a bullish sign. However, the relative strength index (RSI) is flashing caution. In mid-May 2026, the RSI was near 90. That is a rare and overbought level. When the RSI climbs that high, a pullback or sideways period often follows.

Now let’s talk volume. Cisco stock has seen strong buying during its uptrend. But around earnings, you need to watch for distribution patterns. Big institutional investors often take profits after a huge run. A spike in volume on a red day is a warning signal.

Support levels matter just as much. Based on recent price action and options open interest, the key resistance level near $95.98 has been tested, as TradersUnion noted in early May. But by June, price had broken much higher, reaching a daily high of $129.42 on June 2, 2026, per Robinhood. So the resistance zone has moved up.

For traders, the Barchart Cheat Sheet can help spot where price might find support or resistance. Blue areas below the current price act as support. Red areas above are resistance. Right now, the $120-$125 range looks like a key support zone.

If you want to filter out the noise and track Cisco’s moves with a clear approach, learning to stop chasing noise and monitor stock moves with a repeatable framework will help you stick to a plan.

For daily market signals and AI-driven analysis that can sharpen your technical edge, The Deep View Newsletter delivers the data you actually need.

Institutional and Analyst Sentiment

Now that we have seen how the price charts look, let’s check what the big money thinks about cisco stock. Analysts and institutions watch this stock closely, and their moves can tell you a lot.

First, the analyst community is mostly bullish. According to Public.com, 16 analysts give Cisco Systems a consensus rating of Buy, with an average price target of $117.81. But here is the thing. The stock has already blown past that target, trading near $128 in early June 2026. Some analysts are raising their targets fast. For example, HSBC nearly doubled its price target from $77 to $137 in a single note, as reported by TheStreet. That kind of upgrade tells you the AI story is making analysts take notice.

Now, what about big institutions like Vanguard and BlackRock? They are the largest holders of Cisco stock, and their 13-F filings show how they adjust positions each quarter. In the latest filings, some hedge funds added to their Cisco holdings after the AI breakout. Others took profits after the huge run. You can often spot these shifts by looking at the filings, but it takes time. A better way is to filter Yahoo Finance news for big tech market insights without the noise to catch the important updates on institutional moves.

Finally, insider trading. Cisco’s C-suite has been selling small amounts of stock recently. That is not unusual after a 99% rally. Executives often sell for tax planning or diversification. But you should watch for any sudden large sales from the CEO or CFO. So far, nothing alarming has appeared.

To sum up, the sentiment is positive but cautious. The stock is above most price targets, so future moves depend on earnings and AI growth. To keep up with daily market signals and analyst upgrades, consider getting clear AI-driven insights from The Deep View Newsletter.

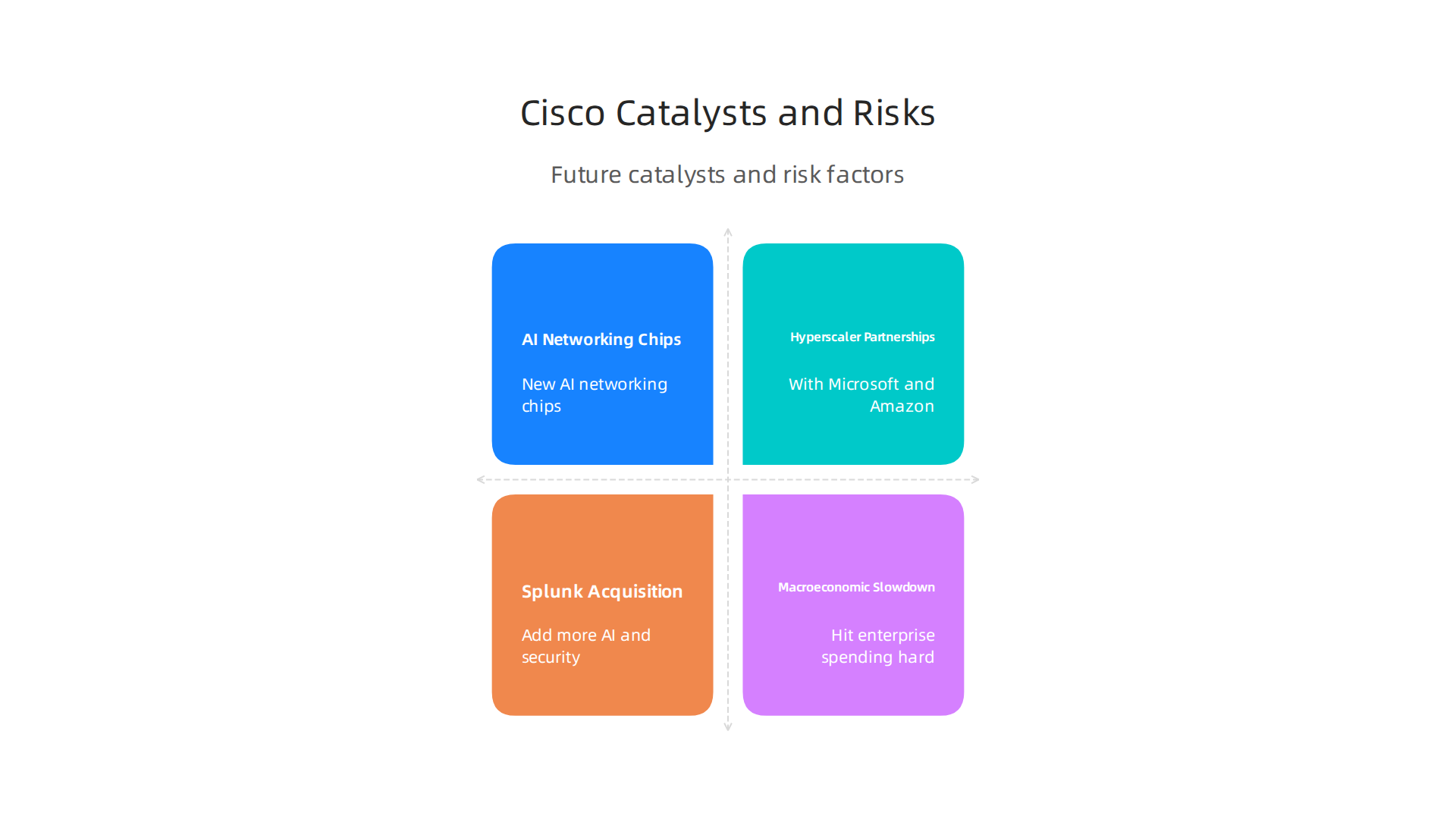

Future Catalysts and Risk Factors for Cisco Stock

So what could push cisco stock even higher from here? And what might send it lower? Let’s break down the catalysts and risks every investor should watch.

Upcoming Catalysts

Cisco is riding the AI wave hard. In the third quarter of fiscal 2026, the company reported revenue of $15.3 billion and guided for full-year revenue of $62.8 billion to $63.0 billion, according to its official earnings release. A big chunk of that growth comes from new AI networking chips and partnerships with hyperscalers like Microsoft and Amazon. Analysts are paying attention. HSBC nearly doubled its price target on Cisco from $77 to $137, as TheStreet reported. Pending acquisitions, like the Splunk deal, could also add more AI and security muscle. For a broader look at which big tech stocks are making big moves today, check out our list of biggest movers today in big tech stocks for 2026.

Risk Factors to Watch

But there are real risks. A macroeconomic slowdown could hit enterprise spending hard. Cisco is also dealing with cost pressures on its supply chain, as noted by Investing.com. Then there is competition from white-box switches. These cheaper alternatives from companies like Arista could eat into Cisco’s market share over time.

Another risk is the US-China trade situation. While export controls on semiconductors have cooled down in 2026, according to East Asia Forum, the threat of new rules is always there. Cisco sells a lot of gear globally, and any disruption could hurt.

Valuation Check

Right now, Cisco’s P/E ratio sits above its 5-year average but is still reasonable compared to faster-growing tech peers like Alphabet (GOOGL). It’s not the wild speculation you see with gamestop stock. And unlike defensive names like jnj stock, Cisco offers growth potential plus a solid dividend. That balance is why many investors see it as a core holding.

To keep track of these catalysts and risks as they unfold, consider subscribing to The Deep View Newsletter. It delivers clear daily AI and tech insights straight to your inbox.

Summary

Cisco’s 2026 story is one of transformation: the company has moved from a steady networking vendor to a central player in AI infrastructure, with AI-related orders topping $1.3 billion and Q2 revenue rising to $15.3 billion. The article explains how Cisco’s custom chips and Nexus Hyperfabric are meeting the needs of hyperscale AI clusters, why raised guidance to $62.8–63.0 billion matters, and how that performance re-rates the stock. It compares Cisco’s positioning against Arista and Juniper, highlights enterprise budget shifts toward AI-ready and secure networking, and flags key regulatory risks like export controls, EU data rules, and tariffs. The piece also covers technical chart signals—moving averages, RSI, and support zones—plus analyst upgrades, institutional flows, and insider activity that influence short-term moves. Readers learn which catalysts could push the stock higher, what risks to watch, and practical ways to filter market noise when monitoring Cisco alongside other big tech names.